Implied Volatility Surfaces from Call Options data¶

Overview¶

We demonstrate some rudimentary techniques in analysis, and modeling of derivative assets, namely call options. The primary themes of the study are: Quantitative Modeling, Black-Scholes Formula, Data Mining, Data Cleaning, Numerical Methods, Regression.

Our objective is to directly calculate the implied volatility of a stock price from observing the pricing of its derivative call options. We'll numerically solve this value from the Black-Scholes Formula for a series of suitable call options on General Mills stock. The volatility thus predicted is not a constant value, but varies significantly with the option's moneyness, $M$, and time to expiration, $T$. Over these abscissae it produces a characteristic "smile" shape on a surface.

European Call Options¶

European call options are contracts that give the holder the right to purchase a stock at an agreed upon expiration date, at a pre-agreed upon price, called the "strike price" $K$. An investor can profit from holding a call option, if the stock price, $S$, is greater than the strike at expiry. This is said to be "in-the-money", $\frac{S}{K} = M > 1$. Otherwise, the option is worthless, since you may as well buy the stock for its market price, in this case it is said to be "out-of-the-money", $M<1$. The obvious question follows, how to price this call option on the market, taking into account all its possible payouts. We will discuss the Black-Scholes Formula below which provides an arbitrage free estimate of the call's market price, $C$.

System Data, Cleaning, and Considerations for Implied Volatility¶

This study is carried out on an options chain declared on General Mills (ticker symbol GIS). You can immediately view a table of all such options being traded on the market on yahoo finance. We can implement a few basic utilities from the yfinance package by Ran Aroussi to pull real time stock and options data directly into pandas DataFrames.

From experimentation, not all options on the list are compatible with the Black-Scholes model in this study, the data may be faulty because there are some contracts which are simply not being traded or are otherwise regarded as completely worthless. Others still are priced outside the admissible interval given by Black-Scholes, in which case solving for volatility will return $\pm \infty$ or other nonsense.

Yahoo Finance already tabulates their estimate for implied volatility, which provides a benchmark by which to examine our results. As yahoo finance will no doubt be using some more sophisticated models than we have for this study. We therefore need not seek numerical agreement with yahoo finance listed implied volatility, but rather we would like to observe the same qualitative behavior in our study. In the final results below you will see both a surface for our computed volatilities and those tabulated on yahoo finance.

# !pip install yfinance

import pandas as pd

import numpy as np

from scipy.stats import norm

import yfinance as yf

# --- My Programs ---------------------------------------------

# import BlackScholesFunctions as BSF

# from BlackScholesFunctions import solve_for_iv

# from OptionsScraper import download_options_chaioptionn, todays_price #-- utilities from the yfinance package by Ran Aroussi

# -------------------------------------------------------------

from matplotlib import pyplot as plt

def download_options_chain(symbol):

tk = yf.Ticker(symbol)

# Expiration dates

exps = tk.options

# Get options for each expiration

options = pd.DataFrame()

for e in exps:

opt_e = tk.option_chain(e)

tempframe = pd.concat( [opt_e.calls, opt_e.puts ] )

tempframe['expirationDate'] = e

options = pd.concat( [options, tempframe], ignore_index=True)

# Bizarre error in yfinance that gives the wrong expiration date

# Add 1 day to get the correct expiration date

options['expirationDate'] = pd.to_datetime(options['expirationDate']) + pd.Timedelta(days = 1)

options['dte'] = options['expirationDate'].map( lambda x: (x - pd.Timestamp.today()).days / 365 )

# Boolean column if the option is a CALL

options['CALL'] = options['contractSymbol'].str[4:].apply(

lambda x: "C" in x)

options[['bid', 'ask', 'strike']] = options[['bid', 'ask', 'strike']].apply(pd.to_numeric)

options['mark'] = (options['bid'] + options['ask']) / 2 # Calculate the midpoint of the bid-ask

# Drop unnecessary and meaningless columns

options = options.drop(columns = ['contractSize', 'currency', 'change', 'percentChange', 'lastTradeDate', 'lastPrice'])

return options

def todays_price( symbol ):

# for example just take the open price

tk = yf.Ticker(symbol)

stockprice = tk.info['open']

return stockprice

now import and filter the table of values appropriately:

- only call options, (remove puts)

- remove the options noone is trading on

- remove the options having $C>S$, as they will have no solution in B-S formula

symbol = "GIS"

stock_price = todays_price(symbol)

dividend_rate = 0.04 #< do we want to set a value for this?

df = download_options_chain(symbol)

# Only analyze the call options

df.drop(df[df.CALL==False].index, inplace=True)

# # Remove options with moneyness > 3.5

# df.drop(df[stock_price/df.strike > 3.5].index, inplace=True)

# # Remove options priced too low

price_lower_threshold = 0.05

df.drop(df[df.mark < price_lower_threshold].index, inplace=True)

# # See to it we remove list items which are outside the analytical bounds of the model

X = (df.mark > stock_price)

#Reset indicies in order

df.reset_index( drop=True, inplace=True )

Reading this table¶

- strike: as above, $K$, the price at which the option holder may choose to buy the stock at expiration

- bid: the most recent bid from a buyer

- ask: the most recent ask from a seller

- volume: quantity of this option traded in a period

- impliedVolatility: as above, the volatility implied by the option price

- expirationDate: when the option holder may exercise

- dte: time until experation in years, $T$

- mark: market price, $C$, we use this in our calculation

print("todays date is", pd.Timestamp.today())

print("todays price of", symbol,"is $", stock_price)

print("no. options in chain: ",df.shape[0])

print("")

#df.sort_values(by='mark').head(23)

df.head(15)

todays date is 2025-10-13 17:53:20.980839 todays price of GIS is $ 49.05 no. options in chain: 179

| contractSymbol | strike | bid | ask | volume | openInterest | impliedVolatility | inTheMoney | expirationDate | dte | CALL | mark | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | GIS251017C00032500 | 32.5 | 15.20 | 17.50 | 2.0 | NaN | 2.775394 | True | 2025-10-18 | 0.010959 | True | 16.350 |

| 1 | GIS251017C00035000 | 35.0 | 12.90 | 14.80 | 2.0 | 1.0 | 2.367192 | True | 2025-10-18 | 0.010959 | True | 13.850 |

| 2 | GIS251017C00037500 | 37.5 | 10.40 | 12.60 | 3.0 | 3.0 | 2.109380 | True | 2025-10-18 | 0.010959 | True | 11.500 |

| 3 | GIS251017C00040000 | 40.0 | 8.10 | 9.30 | 1.0 | 5.0 | 1.478518 | True | 2025-10-18 | 0.010959 | True | 8.700 |

| 4 | GIS251017C00042500 | 42.5 | 3.90 | 5.90 | 1.0 | 2.0 | 0.875001 | True | 2025-10-18 | 0.010959 | True | 4.900 |

| 5 | GIS251017C00045000 | 45.0 | 3.20 | 3.60 | 18.0 | 19.0 | 0.568364 | True | 2025-10-18 | 0.010959 | True | 3.400 |

| 6 | GIS251017C00047500 | 47.5 | 1.05 | 1.25 | 238.0 | 64.0 | 0.397467 | True | 2025-10-18 | 0.010959 | True | 1.150 |

| 7 | GIS251017C00050000 | 50.0 | 0.20 | 0.25 | 1550.0 | 6974.0 | 0.385748 | False | 2025-10-18 | 0.010959 | True | 0.225 |

| 8 | GIS251017C00055000 | 55.0 | 0.00 | 0.10 | 14.0 | 4149.0 | 0.621098 | False | 2025-10-18 | 0.010959 | True | 0.050 |

| 9 | GIS251017C00057500 | 57.5 | 0.00 | 0.20 | 1.0 | 1254.0 | 0.890626 | False | 2025-10-18 | 0.010959 | True | 0.100 |

| 10 | GIS251017C00075000 | 75.0 | 0.00 | 0.20 | 1.0 | 54.0 | 1.859376 | False | 2025-10-18 | 0.010959 | True | 0.100 |

| 11 | GIS251017C00080000 | 80.0 | 0.00 | 0.60 | 3.0 | 6.0 | 2.496098 | False | 2025-10-18 | 0.010959 | True | 0.300 |

| 12 | GIS251121C00027500 | 27.5 | 19.00 | 22.90 | 75.0 | 0.0 | 1.062505 | True | 2025-11-22 | 0.106849 | True | 20.950 |

| 13 | GIS251121C00032500 | 32.5 | 14.10 | 18.00 | 3.0 | 5.0 | 0.845705 | True | 2025-11-22 | 0.106849 | True | 16.050 |

| 14 | GIS251121C00035000 | 35.0 | 12.10 | 14.00 | NaN | 6.0 | 0.888673 | True | 2025-11-22 | 0.106849 | True | 13.050 |

The Black-Scholes Formula¶

The call option price is given, according to the model, as

\begin{equation} C(S,T) = S e^{-qT} N(d_1) - K e^{-rT} N(d_2) , \end{equation}

where $N(x)= \frac{ 1 }{ \sqrt{2 \pi} } \int_{-\infty}^{x} e^{-\frac{z^2}{2} } \ dz $ is the cumulative distribution function of the standard normal, and

\begin{align} d_1 &= \frac{\log\left(\frac{S}{K}\right) + \left(r-q+\frac{\sigma^2}{2} \right) T }{\sigma \sqrt{T}} , \\ d_2 &= d_1 - \sigma\sqrt{T} . \end{align}

Here we have several variables and model parameters, most of which are, in principle, very easy to estimate.

- $C$ : Call option price

- $S$ : Price of underlying asset

- $K$ : Strike

- $q$ : Dividend rate of underlying asset

- $r$ : Characteristic risk-free interest rate

- $T$ : Time to expiration

- $\sigma$ : volatility

Volatility vs Implied Volatility¶

Volatility is a tricky component which is part of a simplified model that treats the stock price as a compound brownian motion process. It is therefore not an observable quantity, and in practice a stock will not obey this drift-diffusion behavior over long periods of time. We can, however, estimate a meaningful value by solving the Black-Scholes formula numerically for the unknown $\sigma$. This framework essentially treats the prices $C$ as market signals which implicitly reveal the opinions of traders as to the volatility of the underlying stock.

Our solution will find strongly varying values of $\sigma$ for each option, which we refer to as "implied volatility". Assigning a volatility to each option seems counterintuitive since we discussed that volatility is rather a property of the underlying asset. However, it also signals how much the market price of the option is deviating from that of Black-Scholes. We also find that market demand drives up both the price and the volatility. Implied volatility is an important metric for hedge funds who desire to profit from irregularly priced options.

Analytical Consequences of the B-S formula¶

The following can be easily proved using only differential calculus, and give certain expectations for the behavior of $C$ and $\sigma$ and the subsequent numerical solution.

- a sufficient condition for the monotonicity of $C$ is if the following holds, $ \sigma^2 > \frac{2\log\left(\frac{S}{K}\right)}{T} + 2(r-q)$, in which case $C$ is guaranteed to be strictly increasing with $\sigma$. Corroborating our expectation that higher market prices will necessarily be on those options with higher implied volatility.

Let $\tilde{S} = S e^{-qT}$ and $\tilde{K} = K e^{-rT}$,

- if the option is in-the-money, $S>K$, the following hold

- the price is bounded from above and below, $ \tilde{S}-\tilde{K} \leq C(S,T) \leq \tilde{S}$

- furthermore, as $\sigma \rightarrow 0$ we have $C(S,T) \rightarrow \tilde{S}-\tilde{K}$

- in the other direction, $\sigma \rightarrow \infty$ implies $C(S,T) \rightarrow \tilde{S}$

- if the option is out-of-the-money, $S<K$, the following hold

- the price is bounded from above and below, $ 0\leq C(S,T) \leq \tilde{S}$

- furthermore, as $\sigma \rightarrow 0$ we have $C(S,T) \rightarrow 0$, and this option is clearly worthless without any volatility to gamble on.

- in the other direction, $\sigma \rightarrow \infty$ implies $C(S,T) \rightarrow \tilde{S}$

- These facts together reproduce the time-boundary conditions of the Black-Scholes model: at expiration $ C(S,0) = \max\{ 0, S-K \}$

Solution Technique¶

We solve for the value of $\sigma$ which makes the output of the Black-Scholes formula match the market price from data. We estimate $\sigma$ numerically using newtons method, and a hybrid implementation of the bisection method to overcome overshooting from newtons method. This does however lead to a downside where one has to filter out deficient results that run away to infinity.

#------------------------------------------------------------

def call_option_price( S, K, T, r, sigma, q=0 ):

if T==0:

C = max(S-K,0)

return C

if sigma == 0:

C = max( S * np.exp(-q*T) - K *np.exp(-r*T) , 0 )

return C

d1 =( np.log(S/K) + ( r - q + 0.5 * sigma**2 ) * T )/( sigma*np.sqrt(T) )

d2 = d1 - sigma*np.sqrt(T)

C = S * np.exp(-q*T) * norm.cdf( d1, 0,1 ) - K *np.exp(-r*T) * norm.cdf( d2, 0, 1 )

return C

#------------------------------------------------------------

#------------------------------------------------------------

def loss_fn( C, S, K, T, r, sigma, q=0 ):

return call_option_price( S, K, T, r, sigma, q) - C

def loss_grad_fn( C, S, K, T, r, sigma, q=0, epsilon=0.0005):

f = lambda ss: loss_fn( C, S, K, T, r, ss, q )

return ( f(sigma+epsilon) - f(sigma) )/( epsilon )

#------------------------------------------------------------

#------------------------------------------------------------

def solve_for_iv( C, S, K, T, r, sigma_guess=1.0, Niter=20, ftolerance=0.0005, q=0, verbose=False ):

if T==0:

converged = True

return np.nan

converged = False

sigma = sigma_guess

f = lambda sig: loss_fn( C, S, K, T, r, sig, q=q)

df = lambda sig: loss_grad_fn( C, S, K, T, r, sig, q=q)

# compute with newtons method

for n in range(Niter):

loss = f( sigma )

if verbose:

print("Itr ", n, ", f_loss =", loss, ", sigma = ", sigma )

if abs(loss)<ftolerance:

converged = True

if verbose:

print("Converged!")

break

else:

loss_grad = df( sigma )

if loss_grad == 0.0:

# default to bisection

if loss > 0:

sigma = sigma/2

else:

sigma = sigma*2

else:

#Newton

sigma0 = sigma - loss/loss_grad

# default to bisection if falls below zero

# or goes to infinity just double it

if sigma0 < 0:

sigma = sigma/2

elif sigma0 == np.inf:

sigma = 2*sigma

else:

sigma = sigma0

#if converged:

# pass

#else:

# print("did not converge in", Niter, "iterations. Final error delta_C =", loss )

return sigma

#------------------------------------------------------------

#------------------------------------------------------------

def show_iv_solution_on_graph( C, S, K, T, r, sigma_soln, smax=-1, q=0 ):

from matplotlib import pyplot as plt

f = lambda sig: call_option_price( S, K, T, r, sig )

smin = 0.0

if smax == -1:

smax = 100.0

s = np.linspace(smin,smax,100)

y = 0*s

for i in range(len(s)):

y[i] = f(s[i])

plt.figure()

plt.plot( s, y )

plt.plot( [smin, smax], [C,C], '--' )

plt.plot( sigma_soln, f(sigma_soln), 'o' )

plt.xlabel("$\sigma$")

plt.ylabel("$C_{BS}(\sigma)$")

plt.legend(["$C_{BS}(\sigma)$","$C_{market}$","$\sigma_{implied}$"])

plt.show()

# Does our method work?

# Check it agrees with the implied volatility in the dataframe

if True:

myRow = df[df.mark > stock_price-df.strike].iloc[0]

sigma_real = myRow["impliedVolatility"]

S = stock_price

K = myRow["strike"]

T = myRow["dte"]

r = 0.06 #some number for interest rate

q = dividend_rate

C = myRow["mark"]

print("Example of soln for implied volatility:")

print(" system vars: S =",S,", K =",K,", T =",T,", r =",r,",")

print(" sigma_real =",sigma_real,", C =",C)

print("")

print("iteratively solve for sigma: ")

sigma = solve_for_iv( C, S, K, T, r, sigma_guess=8.8, q = q, verbose = True )

print("implied sigma estimated = ", sigma )

print("final error in sigma = ", abs( sigma-sigma_real ) )

show_iv_solution_on_graph( C, S, K, T, r, sigma, q=q, smax = 6.0 )

Example of soln for implied volatility:

system vars: S = 49.05 , K = 50.0 , T = 0.010958904109589041 , r = 0.06 ,

sigma_real = 0.3857483300781249 , C = 0.225

iteratively solve for sigma:

Itr 0 , f_loss = 16.877102364531797 , sigma = 8.8

Itr 1 , f_loss = 8.329040081706596 , sigma = 4.4

Itr 2 , f_loss = -0.033335146584594716 , sigma = 0.25884158062834217

Itr 3 , f_loss = 0.0005925291107825303 , sigma = 0.27943522513880337

Itr 4 , f_loss = 3.798208375316303e-07 , sigma = 0.27908164284534187

Converged!

implied sigma estimated = 0.27908164284534187

final error in sigma = 0.10666668723278305

#

# well, we're just gonna send it

#

S = stock_price

K = df.loc[:,"strike"].to_numpy( )

T = df.loc[:,"dte"].to_numpy( )

r = 0.07 #some number for interest rate

q = dividend_rate

C = df.loc[:,"ask"].to_numpy( )

M = S/K

sigma_implied = np.zeros( len(K) )

for i in range( len(K) ) :

sigma_implied[i] = solve_for_iv( C[i], S, K[i], T[i], r, q = q, sigma_guess=9.0, verbose = False )

df.loc[i,'calculated sigma implied'] = sigma_implied[i]

df.sort_values(by='mark').head(8)

| contractSymbol | strike | bid | ask | volume | openInterest | impliedVolatility | inTheMoney | expirationDate | dte | CALL | mark | calculated sigma implied | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 57 | GIS260116C00077500 | 77.5 | 0.00 | 0.10 | 1.0 | 160.0 | 0.449224 | False | 2026-01-17 | 0.260274 | True | 0.050 | 0.430997 |

| 8 | GIS251017C00055000 | 55.0 | 0.00 | 0.10 | 14.0 | 4149.0 | 0.621098 | False | 2025-10-18 | 0.010959 | True | 0.050 | 0.703850 |

| 24 | GIS251121C00060000 | 60.0 | 0.00 | 0.10 | 3.0 | 38.0 | 0.373053 | False | 2025-11-22 | 0.106849 | True | 0.050 | 0.002063 |

| 23 | GIS251121C00057500 | 57.5 | 0.00 | 0.10 | 29.0 | 279.0 | 0.315437 | False | 2025-11-22 | 0.106849 | True | 0.050 | 0.287352 |

| 54 | GIS260116C00070000 | 70.0 | 0.00 | 0.15 | 49.0 | 933.0 | 0.395514 | False | 2026-01-17 | 0.260274 | True | 0.075 | 0.375154 |

| 37 | GIS251219C00070000 | 70.0 | 0.00 | 0.20 | 1.0 | 1.0 | 0.495122 | False | 2025-12-20 | 0.183562 | True | 0.100 | 0.472979 |

| 56 | GIS260116C00075000 | 75.0 | 0.00 | 0.20 | 1.0 | 1222.0 | 0.475591 | False | 2026-01-17 | 0.260274 | True | 0.100 | 0.455315 |

| 162 | GIS270115C00110000 | 110.0 | 0.05 | 0.15 | 10.0 | 27.0 | 0.340827 | False | 2027-01-16 | 1.257534 | True | 0.100 | 0.323773 |

# () - A quick check on my T moneyness plane

plt.figure()

plt.plot( T, M, 'o' )

plt.xlabel("Time to Expiration (yr)")

plt.ylabel("Moneyness (S/K)")

plt.title("Where does our data live in the plane?")

plt.show()

# # Uncomment this to search for extreme values of sigma_implied

#plt.figure()

#plt.plot( T, sigma_implied, 'o' )

#plt.xlabel("Time to Expiration (yr)")

#plt.ylabel("sigma implied")

#plt.title("Results of implied volatility computation")

#plt.show()

Remarks¶

This chart is nothing more than the data loci of our two independent variables $M=S/K$ and $T$, verifying that after all the filtering, we still have some meaningful datapoints that span the plane.

M_cutoff = 5.0

T_cutoff = 1.6

indic = (M<M_cutoff) * (T<T_cutoff)

fig = plt.figure()

ax = fig.add_subplot( 111, projection='3d')

surf = ax.plot_trisurf( M[indic], T[indic], C[indic]

, cmap="YlGnBu"

, antialiased=True

, alpha = 0.90

, linewidth=0.1

, edgecolor="k"

)

cbar = fig.colorbar(surf, ax=ax)

cbar.set_label("Price: C")

#ax.set_ylim([0,1])

ax.set_xlabel("Moneyness (S/K)")

ax.set_ylabel("Time to Expiration [yr]")

ax.set_zlabel("Price: C")

plt.title("Price Surface")

ax.view_init(elev=20, azim=45)

# plt.tight_layout()

plt.show()

Remarks¶

This chart for the option prices matches the basic shape we expect from the analytical B-S formula

#

# Surface

#

# M_cutoff = 3.3

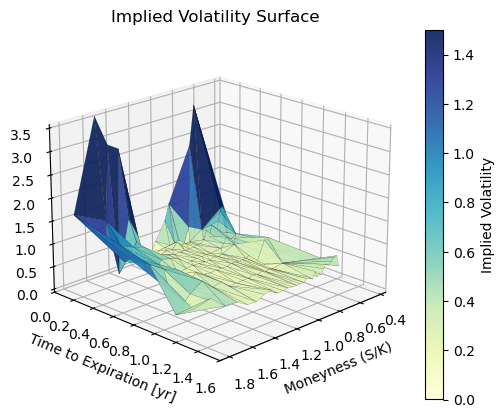

sigma_cutoff = 5

indic2 = indic * ( sigma_implied < sigma_cutoff )

fig = plt.figure()

ax = fig.add_subplot( 111, projection='3d')

surf = ax.plot_trisurf( M[indic2], T[indic2], sigma_implied[indic2]

, cmap="YlGnBu"

, antialiased=True

, vmax = 1.5

, alpha = 0.90

, linewidth=0.1

, edgecolor="k"

)

cbar = fig.colorbar(surf)

cbar.set_label("Implied Volatility")

ax.set_ylim([0,T_cutoff])

ax.set_xlabel("Moneyness (S/K)")

ax.set_ylabel("Time to Expiration [yr]")

ax.set_zlabel("Implied Volatility")

plt.title("Implied Volatility Surface")

ax.view_init(elev=20, azim=45)

# plt.tight_layout()

plt.show()

Remarks¶

This is the calculated implied volatility. Observe, for a slice of constant $T$, we have the characteristic U-shaped "volatility smile" in the $M=S/K$ variable. In the flatter regions, around $T \geq 0.8$, local hills and spikes are considered points of interest, and may be targets for investigation of mispriced options.

sigma_yahoofinance = df.loc[:,"impliedVolatility"]

fig = plt.figure()

ax = fig.add_subplot( 111, projection='3d')

surf = ax.plot_trisurf( M[indic2], T[indic2], sigma_yahoofinance[indic2]

, cmap="YlGnBu"

, antialiased=True

, vmax = 1.5

, alpha = 0.90

, linewidth=0.1

, edgecolor="k"

)

cbar = fig.colorbar(surf)

cbar.set_label("Implied Volatility")

ax.set_ylim([0,T_cutoff])

ax.set_xlabel("Moneyness (S/K)")

ax.set_ylabel("Time to Expiration [yr]")

ax.set_zlabel("Implied Volatility")

plt.title("Implied Volatility Surface, from yahoo finance")

ax.view_init(elev=20, azim=45)

# plt.tight_layout()

plt.show()

Remarks¶

This is the surface for the implied volatility provided by yahoo finance data. It qualitatively matches our calculation.